3 Testing the efficient markets hypothesis

The most basic test of market efficiency is to examine whether the price of the asset equals its fundamental value. For example, does the value of a stock in a company equal the present value of expected future dividends?

3.1 The joint hypothesis problem

But as noted earlier, determining the fundamental value, or indeed any measure of the value of an asset, requires the flow of future payments to be discounted for risk. But what is the correct risk adjustment? As this is usually not known, this requires an assumption of the right model of risk.

Therefore, tests of the efficient markets have a challenge. If a test rejects the proposition that a market is efficient, is this because the efficient markets hypothesis does not hold in that market, or is it because we have not used the right model of risk? This question is known as the joint hypothesis problem.

Much of the debate about market efficiency that we are about to cover ultimately hinges on whether the assessments of market efficiency have used an appropriate model of risk.

3.2 The event study methodology

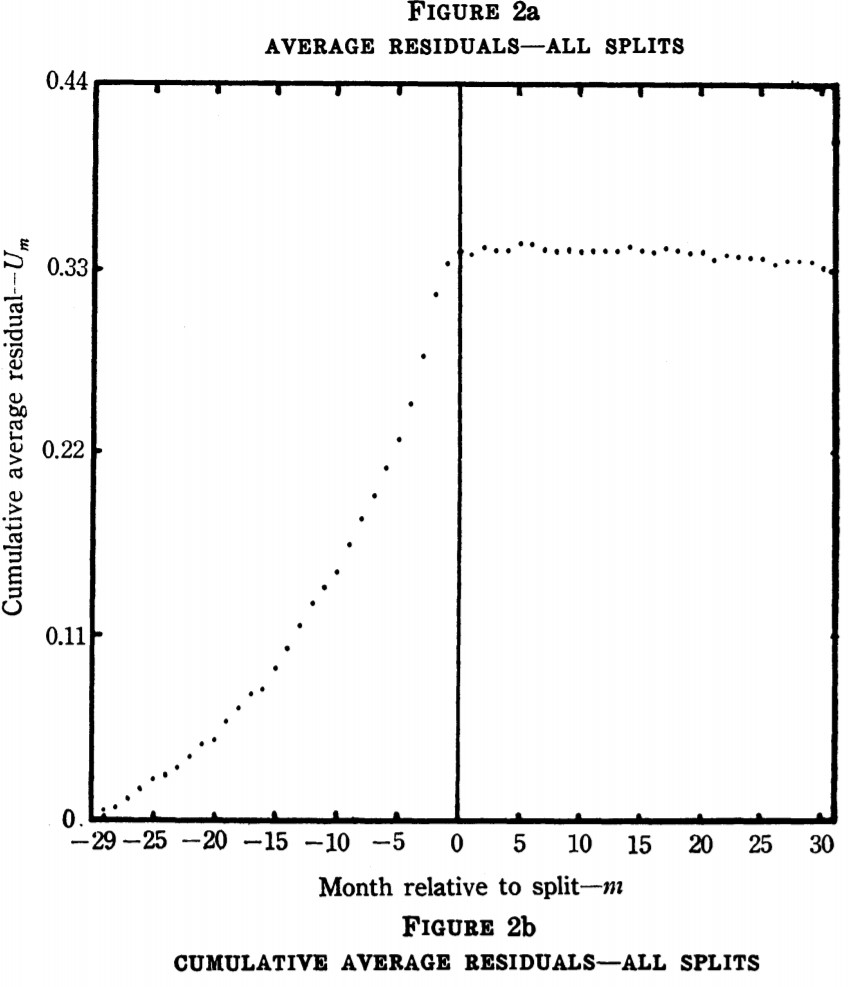

One classic test of the efficient market hypothesis is the event study methodology devised by Ball and Brown (1968). To test efficiency, look at a class of events that affect the price of stocks (e.g. earnings announcements) and examine the returns in the days leading up to the event, on the day of the event, and in the days after the event.

If markets are efficient, we should see a reaction to the event (e.g. good or bad news) in the days leading up to and including the event. There should be no further reaction on days after the announcement as an efficient market should react completely in response to the event as soon as the information is available.

The first papers to use event studies to examine market efficiency typically found evidence consistent with the weak and semi-strong forms of the efficient markets hypothesis. In one famous paper pioneering the event study methodology, Fama et al. (1969) examined stock splits, where a company is split into two. They found that prices immediately reflected all available information on announcement of the split, and no abnormal returns were achieved after the announcement (see the image below).