7 Momentum and reversal

The weak form of the efficient markets hypothesis states that returns should not be predictable using past returns. Despite this, there is evidence of medium-term momentum and long-term reversals.

7.1 Momentum

Momentum occurs when returns are positively correlated with past returns. There is reliable evidence that momentum exists over medium-term intervals of three to 12 months.

Jegadeesh and Titman (1993) grouped all New York Stock Exchange stocks traded between 1963 and 1989 into deciles based on their return over the previous six-months. They then calculated the average returns for each decile over the next six months. They found that the top decile of prior winners outperformed the bottom decile by an average of 10% (on an annual basis).

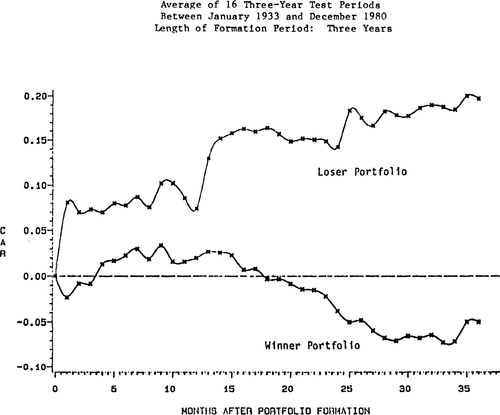

7.2 Reversal

De Bondt and Thaler (1985) ranked all stocks traded on the NYSE for every three years between 1926 and 1982 by their return over those three years. From these they formed a portfolios of 35 “winner” and 35 “loser” stocks and measured their performance over the following three years. They found that over the sample period the average return of the loser portfolio was 8% per year higher than the return of the winner portfolio.

7.3 A behavioural explanation

The combination of momentum and then reversal suggests a combination of under-reaction then over-reaction, phenomena we have already seen in the explanations for lagged reactions to announcements and value-stock out-performance.

There are many attempts to explain this pattern. One proposed by Barberis et al. (1998) involves a combination of anchoring, by which people underweight new information relative to priors, and representativeness.

They proposed that when a company announces surprisingly good earnings, investors react insufficiently, meaning that the price does not increase as much as it should. This lower price, however, means that returns in subsequent periods appear good, creating post-announcement drift. This drift eventually causes people to overreact as they see the short period of good results as representative of the quality of the stock. This overreaction pushes the price too high. That high price then means that returns in following periods appear poor, leading to the eventual reversal.