10 Excessive volatility

If you look at a chart of stock prices, one striking feature is that they are volatile.

Under the efficient markets hypothesis, variation in stock prices should be due to new information. Shifts in prices should also be accompanied by changes in rationally-varying forecasts in dividends.

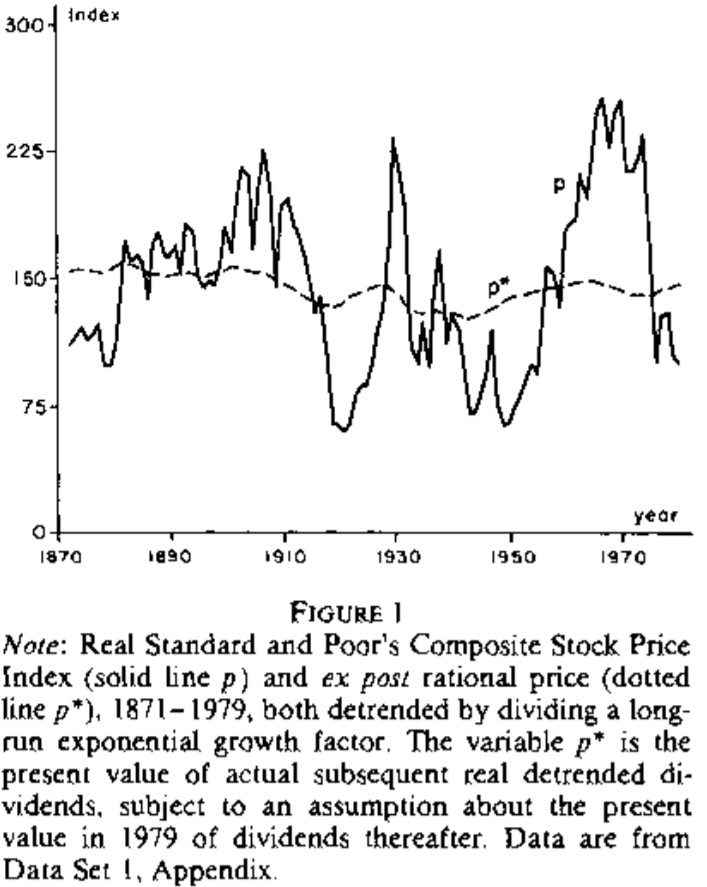

A challenge with testing whether changes in prices are caused by changes in expectations of future dividends is that we don’t know what dividends will be paid in the future. However, Shiller (1981) noted that we could look at past dividends to construct the “ex-post rational stock price” for any point in time given dividends paid from that point in time until today.

You might note that even if we look at past prices and the dividend flows from then on, the expectation relates to the discounted sum of dividend flows through to infinity. We will always lack some information to test whether the price change is justified.

Shiller argued that the ex-post rational stock price should be more volatile than the price itself. This is because future dividends that comprise the ex-post rational stock price will move based on unexpected information - information that investors did not have when the price was set - adding volatility to the ex-post rational stock price that the price itself should not be subject to.

In the chart below, the solid line represents the real Standard and Poor’s Composite Stock Price Index, detrended for long-run growth. The dashed line is the ex-post rational stock price. It is obvious that the volatility of the index is far above that of the ex-post rational stock price.

10.1 Behavioural explanations

There are many explanations for excessive volatility (beyond the plentiful arguments that the volatility is not actually excessive). Many of these are based on similar ideas to the other anomalies that we have discussed.

One relates to representativeness. When an investor sees a short sample of good earnings, they believe that earnings have gone up and will continue to be higher in the future. They therefore over-react. They might also extrapolate past returns too far into the future when estimating future returns, again based on representativeness.

10.2 Further material

If you wish to read further material on behavioural finance, Shiller (2003) is one good starting point.

The following video, an interview with Eugene Fama and Richard Thaler, covers many of the behavioural finance topics discussed in this book.